Joe Deposits 1 500 in an Account That Pays 3 Annual Interest Compounded Continuously

If your investment account earns compound interest, then you are earning interest on interest as well as on your investments. Compound interest is undoubtedly the most important concept to understand when building wealth for the long term. Here's a closer look.

How compound interest works

Compounding is happening when your investment grows each year -- and when the amount that your investment grows by also increases. The value of an investment that generates earnings is compounded by earnings that generate earnings of their own.

It's a relatively simple concept, but one with mind-blowing possibilities. The longer you let your investments grow, the more rapidly they grow.

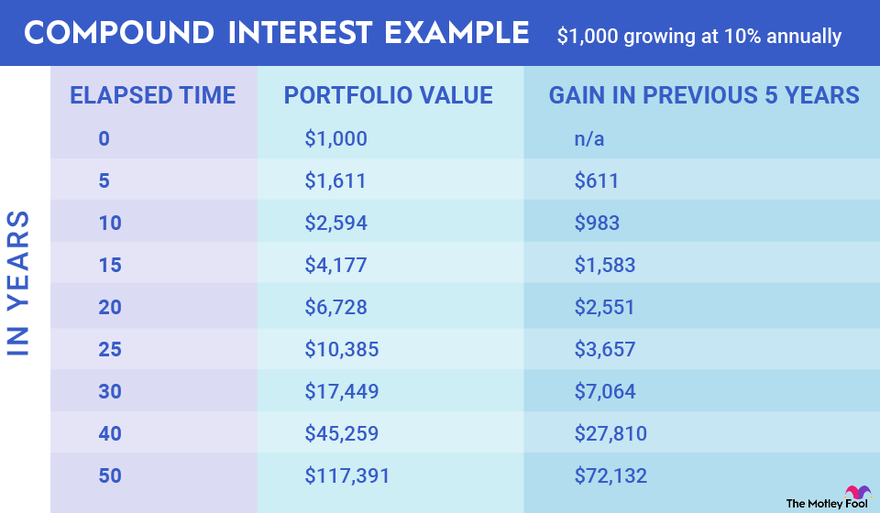

Consider a single $1,000 investment growing at 10% annually:

Image source: The Motley Fool

Notice that over the first five years, the modest $1,000 investment grows by $611. But decades later, without any additional money being invested, that investment is growing by tens of thousands of dollars in the same number of years.

Now imagine what happens if you start with $5,000 or $10,000 and keep contributing more money to your account regularly and making smart investment choices to increase your returns.

Simple interest versus compound interest

While compound interest includes interest earned on previously generated interest, simple interest is just the interest rate multiplied by the investment or principal amount.

Simple interest is often used in a loan or bond context where the interest is the same every period and there is no compounding. Compound interest is used in investment and savings contexts.

The simple interest formula is A = P(1 + RT). (You can find the variables defined in the next section.) This means the account value is equal to the original investment amount times 1, plus the rate multiplied by the time. The simple interest formula isn't as complicated as the compound formula below because it doesn't include the compounding factor.

Compound interest formula

Let's go over the compound interest formula and define each of the variables.

P(1 + R/N)^(NT) = A

- Principal: P is the investment or principal balance at the start of the investment. If you use a spreadsheet or a financial calculator to calculate interest, principal is also known as present value.

- Rate: R is the interest rate earned on the investment.

- Number: N is the number of times per period that interest is compounded. For example, many savings accounts compound monthly but have an annual interest rate.

- Time periods: T is the number of time periods.

- Account value: The formula is used to calculate the account value, A. This variable is also known as future value.

Let's say you invested $10,000 in a savings account offering 1% interest compounding monthly. After five years, you would calculate the savings amount like this:

$10,000(1+.01/12)^(12*5) = $10,512.49

Which types of accounts offer compound interest?

You have several options for taking advantage of compounding interest to build wealth. Each of these investing strategies generates compound interest:

- Savings accounts: Banks lend out the cash that you put into a savings account and pay you interest in exchange for your not withdrawing the funds. Savings accounts that compound daily, as opposed to weekly or monthly, are the best because frequently compounding interest increases your account balance faster. You can open a savings account with any local or online bank.

- Money market accounts: These are mostly the same as savings accounts, except money market accounts allow you to write checks and make ATM withdrawals. Money market accounts often pay slightly higher interest rates than savings accounts. The downsides of money market accounts are that most limit the number of transactions you can complete each month and some charge a fee if your balance falls below a certain amount.

- Zero-coupon bonds: These bonds generate the equivalent of compound interest to compensate for the risk associated with holding zero-coupon bonds. A zero-coupon bond holder purchases a bond at a steep discount, receives no interest payments (coupons) in exchange for holding the bond, and is paid the bond's face value when the bond is due. There is a risk that the company may not be able to repay the bond's full face value at the end of the term.

- Dividend stocks: Stocks that pay dividends generate compound interest if you reinvest the dividends. You can instruct your brokerage to automatically reinvest all dividend payments you receive and buy more shares.

While savings accounts and money market accounts are both extremely safe options, you are unlikely to find an account that pays even 1% interest. To significantly profit from compounding interest, it's important to diversify your money with different types of accounts and investments.

Best Stock Brokers for October 2022

Compound interest in current events

A recent development in compound interest accounts is the rising popularity of I Bonds. I Bonds, or Series I Savings Bonds, are issued directly by the U.S. Treasury and pay interest based on the country's current inflation rate.

The bonds have a low fixed base rate that is paid for the life of the loan and an additional inflation rate that is set twice a year based on the Consumer Price Index (CPI). In August 2022, after a few consecutive months with inflation exceeding 8%, the rate on I Bonds was 9.62%.

I Bonds are certainly an interesting investment -- earning 9.62% on an investment backed by the full faith and credit of the U.S. government is a pretty easy decision. But the bonds really make sense only when inflation is raging. The base rate for bonds issued since May 2000 is 0%, and the last time the base rate was even as high as 1% was 15 years ago. Additionally, prior to the November 2021 rate change, the inflation rate had gone over 2% only four times since September 1998. For comparison, the inflation rate was negative twice over that period.

Finally, the rate is tied to the overall CPI, which means it may still be lower than the inflation you experience in your everyday life. For example, in July 2022, the overall CPI came in at 8.5% for the previous 12 months, but energy prices were up 32.9% and food prices were up 10.9% over the same period.

This means you may end up holding the bond through long periods of poor performance only for it to return less than the inflation on specific items once the rate is actually jacked up.

The power of compounding interest

Compounding interest can turn meager investments into wealth over time, but only if you start investing as soon as possible and then stay invested.

The sooner you start investing, the more time you have for interest to compound on interest. The $1,000 investment in the example above increased by $983 from year 5 to year 10 and by $7,064 from year 25 to year 30. The longer you wait to start investing, the older you are when you reach year 30.

Staying invested is key to maximizing the effects of compound interest. If you're constantly moving or withdrawing your money whenever the market declines, you lose out on a lot of potential compounded interest.

Staying invested can be hard through market drawdowns. If you have a portfolio worth $100,000 and the market drops 20%, it looks as if you lost $20,000. But keep in mind that there are no true losses until you make the decision to sell. If you focus on buying strong businesses that can persist through periods of bad economic performance, the prices will rebound over time.

Too often, investors are scared off by the drawdown and sell, only to then miss the bounce and buy back the stocks once the price has recovered.

Who benefits from compound interest?

Both financial institutions and consumers benefit from compound interest. Banks pay compounding interest to consumers at low interest rates in exchange for their not withdrawing funds and simultaneously lend the deposited money to earn attractive streams of interest income.

Consumers can use compound interest in either the types of accounts discussed above or with stock returns to turn a relatively small nest egg into a healthy retirement account over time.

Related investing topics

Can compound interest make you rich?

Compound interest can turn you into a wealthy person – but not quickly. The effects of compounding interest occur over the long term and only if you prioritize buying and holding as an investor.

The Motley Fool has a disclosure policy.

Source: https://www.fool.com/investing/how-to-invest/stocks/compound-interest-accounts/

0 Response to "Joe Deposits 1 500 in an Account That Pays 3 Annual Interest Compounded Continuously"

Postar um comentário